hi.

I teach my 470,000 TikTok followers and 190,000 Instagram followers how to invest and trade stocks. Wanna learn more? Check the links below:

I teach my 470,000 TikTok followers and 190,000 Instagram followers how to invest and trade stocks. Wanna learn more? Check the links below:

I’ve been on TikTok for over six years. I get a LOT of repeat questions. If I referred you to this page, it’s because you, like hundreds before you, have asked the exact same question, which isn’t a bad thing! You’re all thinking the right way.

If you’re new to investing, bookmark this page and check back here every so often, as I’ll be updating it periodically.

If you want to be a well rounded investor, you might also be interested in grabbing my investing research vault here.

What do you think about Acorns/Robinhood/Fidelity/etc.

I have only ever used TD Ameritrade (now a part of Charles Schwab). I have no thoughts or opinions on any other brokerage. I use Schwab for investing and Think or Swim (through Schwab) for stock trading. I personally love it. All brokerages are basically the same these days. Don’t overcomplicate it.

Which S&P 500 ETF is better?

They are all exactly the same. I own SPYM (formerly SPLG) which has the exact same holdings and the exact same performance of VOO or SPY. At first glance, it feels logical to think that since dividends are paid per share, you’d be better off buying a cheaper ETF like SPYM at around $81 instead of VOO or SPY trading north of $600+ … but the math doesn’t quite work that way. The catch is that all three funds have roughly the same dividend yield, around 1%, which means the dollar amount you earn is driven by how much money you invest, not how many shares you own. For example, 100 shares of VOO at about $633 per share costs roughly $63,300 and pays around $707 per year, while 100 shares of SPY at $688 costs about $68,800 and pays roughly $728 annually. SPYM looks much cheaper at around $81 per share, but 100 shares only costs about $8,100 and pays roughly $91 per year. If instead you invested the same $63,000 into SPYM, you’d end up with around 777 shares, which at $0.91 per share in dividends would generate about $700ish per year—nearly identical to SPY and VOO. So yes, SPYM is cheaper per share, but once you normalize for dollars invested, the dividend income ends up being roughly the same across all three.

3. Why do SPYM (formerly SPLG), VOO, and SPY all have different prices?

This video explains it. But if you’d rather read … If SPYM (formerly SPLG), SPY, VOO, and other S&P 500 funds all invest in the exact same 500 companies, why are their share prices so different? The key misconception is thinking the share price reflects the value of the underlying holdings. It doesn’t. An ETF’s price is determined by its net asset value (NAV), which is calculated by taking the fund’s total assets under management (AUM) and dividing it by the number of shares the fund has issued. Two funds can hold the same stocks in the same proportions, go up the same percentage in a year, and still trade at wildly different prices simply because one issued more shares or started with a lower base price. That’s why SPYM can trade around $81 while SPY is over $688 and VOO is over $633, even though NVDA is the top holding in all three. More shares of NVDA inside a fund doesn’t make it “better” … it just reflects how big the fund is. What actually matters for most investors is accessibility (can you buy whole shares easily?), expense ratios (all are very low, with SPYM being the lowest), and long-term tracking accuracy. Bottom line: different prices, same engine, same results—don’t let the sticker price fool you.

4. What does DCA mean?

DCA = Dollar Cost Average. It’s an investing strategy that says you invest the same amount of money into the same investment every single month (or whatever period of time you choose). For example, you’d invest $583 per month (to hit your annual Roth IRA max of $7,000) into FTEC on the first of every month AND you’d invest $200 into your S&P 500 ETF.

5. Which is better? Lump Sum or DCA?

Lump Sum means you invest one large amount. It’s better if you can afford it because you’re starting from the earliest point with the largest amount, allowing you to compound and earn more money from dividends faster. But most people can’t afford to lump sum, so DCA is perfectly fine. I also personally prefer to do a hybrid during volatile markets, like during recessions. So I start a position, but I don’t spend 100% so I can add even more money when markets drop lower.

6. I’m up X% - when should I take the profit?

First, give this a read. It’s my blog post: 7 Smart Strategies For Taking Profits. You might find the answer here. If not, come back and go through these options:

Why did you invest in the company? What kind of investment is it? Did you invest to hold it for 10-30 years? Then who cares if you’re up 35%. Imagine you bought stock in NVDA 10 years ago and sold it when it went up 35% only to miss out on the 19,500% rally that came after that. Don’t be shortsighted with your profits, especially if it’s meant to be a long term investment.

Remember, as a long term investor, your goal is usually to build very large positions in stocks or ETFs over a 10-30 year period. The goal isn’t to lock in gains and then hope for a crash to hopefully rebuy at a lower price. The goal is to Always Keep Adding.

Here’s an example: I buy 100 shares in a company every single year. Over a 20 year period, I’ve accumulated 2000 shares (we’re also assuming they never issued a stock split or added a dividend.)

Now I’m close to retirement and I want to sell a portion every single year. I might consider then selling 100 shares every year. This also assumes the company is still strong and performing well, even if they’ve shifted from a growth stock to a more stable blue chip stock. If fundamentals have changed, management is bad, etc. then you might opt to sell some (or all).

One last option is to move some funds from the profitable stock into a new position. If you’re overweight one company, you may want to rebalance your portfolio.

As a general guideline, when one stock makes up more than about 10% of your portfolio, it’s worth considering a rebalance because your risk becomes concentrated in that single company. If you’re comfortable with higher risk, 10–15% might be fine, but once it grows to 20% or more, many investors think about trimming.

How much should you sell? That depends entirely on your risk tolerance. You might prefer that position to be closer to 5–10%, but it’s a personal choice. For example, Apple makes up 25% of my portfolio, and I’m comfortable with that level of concentration.

If you bought a high risk speculative stock, technical analysis is your friend (I use the RSI to know when to sell - or buy). You can also watch this video on when to sell a speculative investment and this video on when to sell long term investments.

If you REALLY want to lock in some gains, remember you never have to sell your entire position, you could always sell a quarter of the shares or half - totally your call. There is no one size fits all answer.

7. I’ll have to wait X amount of years to pay back my investment via dividends. On my McDonald’s video, I said it would cost over a million dollars to make $20,000 a year. The natural conclusion (also the wrong conclusion): “So it takes 47 years to pay back your investment??” This is the WRONG WAY to look at dividends. That “47 years to get your money back” take completely misunderstands what dividends are and how stocks work. Dividends are income generated by an asset you still own, not a repayment plan for your original investment. When you buy McDonald’s stock, you’re not lending McDonald’s money and waiting to be paid back—you’re buying a productive asset that can pay you cash while the asset itself appreciates in value over time. In those 47 years, you’re collecting dividends every single year, those dividends usually grow over time and can be reinvested, compounding over and over. At the end you still own the shares, which historically are worth far more than what you paid. Framing dividends as “how long until I break even” is like saying a rental property is bad because rent doesn’t equal the purchase price fast enough—ignoring the fact that the property still exists and usually becomes more valuable.

8. Should I wait for the Recession to Start Investing?

Generally, no, waiting is a loser’s game. This is a dumb idea. Timing the market never works. There are too many hypotheticals. Too many what ifs. When is the recession? Will you know it’s happening or will we all find out after the fact? Will you miss your chance? What if we DO know it’s happening? Will you wait for lower prices? What if they don’t happen? What if markets recover and you missed your chance?

9. What is Collateralized Lending and is it SAFE?

You might have heard of something called BUY, BORROW, DIE on TikTok. It sounds like nearly free money and a great way to avoid paying a huge tax bill ... but it’s more complicated.

Collateralized lending (or a Pledged Asset Line if you use Charles Schwab) is simple once you strip away the confusing investing lingo: you’re borrowing money using your investments as backup instead of selling them. Let’s say you’ve built up a portfolio of stocks or ETFs, and instead of cashing them out, your brokerage lets you borrow against their value. The big benefit is you get access to cash without selling your investments, which means you don’t trigger taxes and you stay invested if the market keeps going up. That’s why some people use it for short-term stuff like a down payment on a home, a new bathroom or kitchen renovation, or even a fancy vacation.

Here’s the thing most people forget and where beginners get caught off guard. When you take out this kind of loan, your brokerage requires you to keep a safety cushion in your account. This is your “buffer.” For example, if you have $100,000 invested and borrow $50,000, you still have $50,000 of your own money in there. If the market drops and your investments fall to $70,000, your loan DOES NOT CHANGE! You still owe $50,000, so your buffer shrinks to $20,000. If that buffer gets too small, your brokerage can step in and force you to either add cash or sell some of your investments. And they won’t wait for the market to recover—they’re protecting their loan, not your long-term plan.

And don’t forget about the interest. Instead of sending in a monthly payment like a typical loan, the interest usually just builds up in your account and gets added to what you owe. You can cover it a few different ways: by adding cash from your bank, using your existing dividend income, or selling a small portion of your shares. All of those are allowed, but they don’t carry the same risk. If you let the interest pile up, your loan balance slowly grows, which makes your situation more fragile if the market drops. Using dividends can work well if your portfolio produces enough income, but relying on selling shares can backfire, especially if stocks are down and you’re forced to sell more than you want.

That’s really the trade-off. On one hand, it’s fast, it’s flexible, and it can be cheaper than other types of loans. And you might avoid some big tax bills! On the other hand, it adds pressure to your investments. Without a loan, a market drop is usually something you can ride out. With a loan, that same drop can force you to act when markets are dropping and everyone is panicking. AKA: The worst time to sell. The safest way to think about it is this: it’s a useful tool, but only if you have a clear plan to manage the risk and cover the costs without relying on the market to bail you out.

And here’s the long term play: some super wealthy investors use this strategy as part of what’s called “buy, borrow, die.” The idea is simple: BUY investments and hold them, BORROW against them when you need cash instead of selling, and then when you DIE, your heirs inherit the investments. Because of special tax rules, the investments get a “stepped-up” value at death, which usually wipes out most of the capital gains taxes. In other words, borrowing lets your money keep growing, and passing it on can help avoid the taxes that would normally hit if you sold. It’s not something everyone does, but it’s the strategy that makes collateralized lending really powerful for long-term wealth planning. But this stuff isn’t for your average retail investor with 100 shares of Apple.

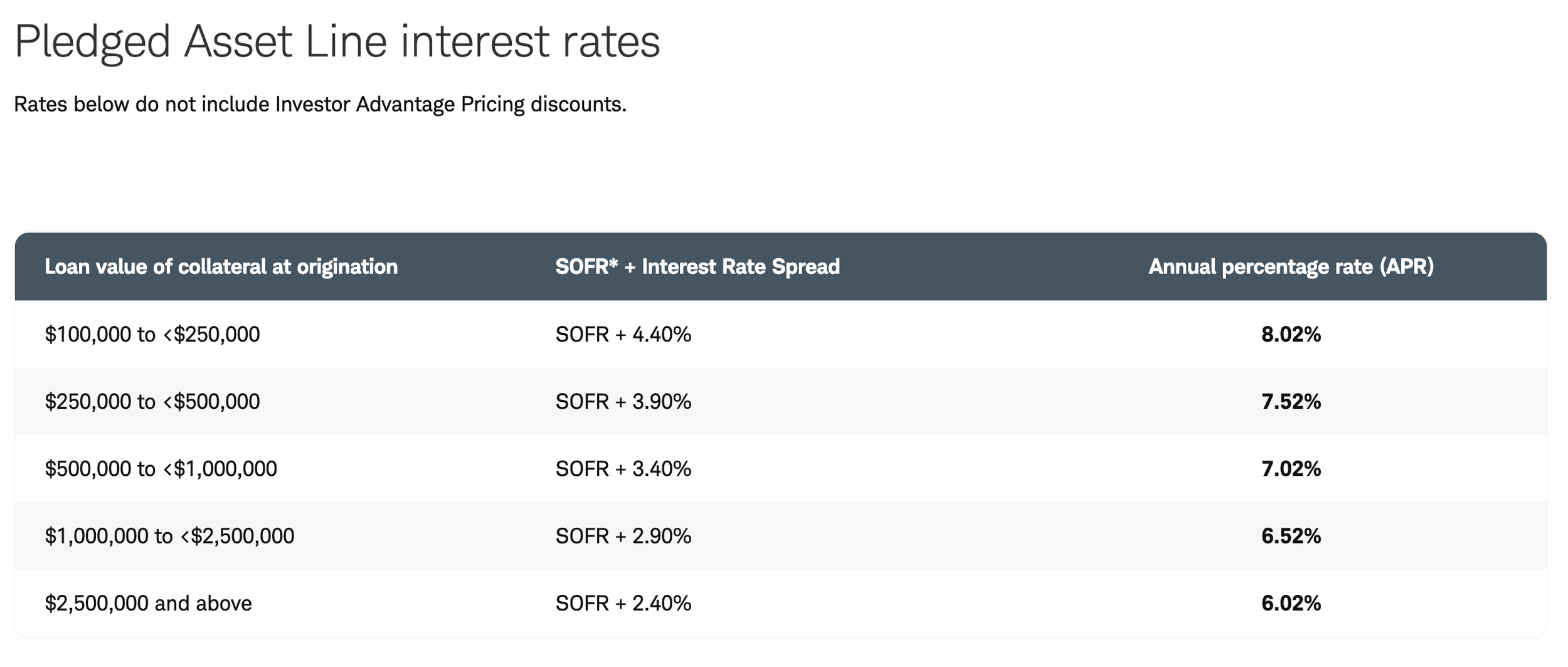

You need a HUGE portfolio to be able to do this. Take a look at this screenshot from Schwab’s Pledged Asset Line page:

If you want to watch some videos on collateralized lending, here are a few links. I know some people learn better from reading, and others learn better from watching:

This video goes all the way back to 2023, and even though TD Ameritrade is no more, the info is still relevant explaining briefly what Buy Borrow Die means

Again, a longer video from 2023 goes into a little more detail about collateralized lending.

10. Why Do I Like a Technology Fund in the Roth IRA and NOT a Dividend Fund?

As always, this comes down to personal preference.

Some investors take the annual Roth IRA contribution limit (currently $7,500 if you're under 50) and split it among several ETFs. Others prefer to maximize the account's tax-free growth potential by concentrating on their highest-conviction investment.

Many investors like dividend funds in a Roth IRA. The logic makes sense: dividends paid in a taxable brokerage account are generally taxable each year, even if you reinvest them. Inside a Roth IRA, those dividends can grow tax-free, and qualified withdrawals in retirement are tax-free.

But let's look at the numbers.

Suppose you invest $7,500 into a dividend ETF yielding 3.2%. That's about $240 per year in dividends.

So the question becomes: are you putting your Roth IRA's most valuable feature—tax-free growth—to work on $240 of annual dividend income, or on an investment that could potentially grow much more over the coming decades?

My thinking is this: while I'm accumulating wealth, I'm not selling my growth investments anyway. If I own a tech ETF in a taxable account, I generally don't owe taxes on the gains unless I sell.

But what happens in retirement?

Let's say your tech ETF has appreciated 1,000% over several decades and you want to sell $100,000 worth of shares.

In a taxable account, a significant portion of that withdrawal could be subject to capital gains taxes.

In a Roth IRA, qualified withdrawals are completely tax-free.

Now compare that to a dividend portfolio generating $20,000 per year in retirement. Yes, receiving that income tax-free is valuable.

But for me, the bigger tax benefit may be shielding six-figure portfolio withdrawals and decades of compounded growth from taxes altogether.

That's why I personally prefer to place my highest-growth investments inside my Roth IRA and hold dividend investments in taxable accounts.

The Roth IRA is the most valuable real estate in my investing life, and I want my fastest-growing assets living there.